On the 23rd March 2020, then Prime Minister Boris Johnson announced the UK’s first national lockdown in reaction to Covid-19. People were only allowed to leave their homes for strictly limited reasons and it was advised that “everyone who can work from home should do so.”

Three years on, the insurance industry has changed dramatically. Arguably, the biggest change has been in hybrid working.

Each class will have had its own challenges and sector-specific claim trends stemming from the global pandemic, especially as we are now beginning to see both the macroeconomic and socioeconomic impacts, not to mention additional regulatory scrutiny by UK regulators. However, hybrid working has affected us all equally.

Most brokers and insurers had to increase the speed of any digitisation plans they had to enable their employees to work from home and overnight become a remote workforce engaging with all their stakeholders virtually.

The impact on the way the insurance industry operated from this first lockdown was immediate and sparked the beginning of the three-year debate in the workplace: can businesses in the insurance sector still thrive with their employees working remotely?

The ‘working from both the office premises and home’ hybrid working model has now had three years to prove itself, and with the economic impacts of Covid-19, the geopolitical landscape and the macroeconomic effects of the ongoing cost of living crisis, commercial real estate is an expensive luxury for many to have. However, it is becoming clear that there is a strong divide between those that do not think video calls are a like-for-like replacement for the traditional nature of the face-to-face business and those that want flexibility.

Some sceptical business leaders say they need workers in the office full-time to foster a collaborative environment. At the other extreme: many employers are letting their employees work from anywhere.

What neither side of the coin can argue with, is the amount of people movement following on from the Great Resignation sparked by the pandemic. The pandemic has been an accelerant for change with many having an abundance of time in order to stop and consider what they want from the workplace.

The EY 2021 Work Reimagined Survey found that 54% of the 16,000 employees they surveyed from around the world, would consider leaving their job post-pandemic if they are not afforded some flexibility to working once they return to the office.

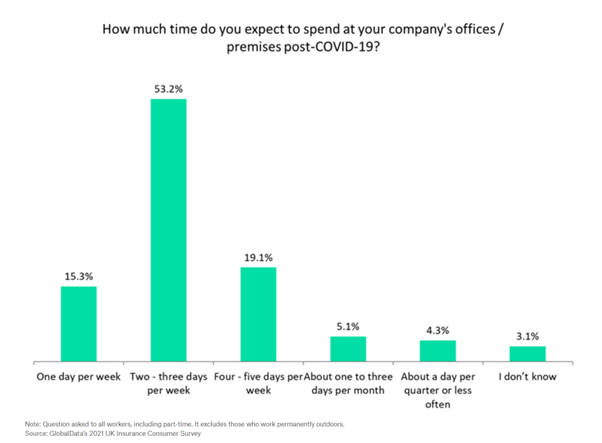

Another survey carried out by GlobalData in 2021 revealed that over 50% of respondents only expected to be in their company’s premises 2-3 days a week post Covid-19.

Insurance professionals are prioritising the implementation of flexible working where caring for staff wellbeing is key. Prioritising talent attraction and retention action as the post-pandemic resignation trend hits and the cost-of-living crisis cripples households.

Insurance businesses need to retain their talent as well as develop ways to train and develop their more junior staff where the traditional methods of learning through osmosis may no longer apply. Top performance becomes hard to achieve without strong wellbeing which is developed through work-based cultures where employees not only feel adequately remunerated, but feel supported, equipped with knowledge and have the skills and behaviour to do their best wherever they chose to work from.

Internal culture will be key. There are many drivers of culture, but the FCA focus on 4 main drivers, these are:

- Purpose – aligning your firm’s values with policies and procedures, including incentive structures

- Leadership – holding your own behaviour to account and being responsible for the behaviour of those that report to you

- Approach to rewarding and managing people – rewarding long-term value creation, not short-term profits. And that means firms treating customers fairly, to their benefit, and that of firms, shareholders and the wider economy

- Governance – whereby governance structures, risk management systems and remuneration, interact with the underlying shared beliefs and individual perceptions of risk culture, and in concert influence performance and outcomes

Concluding thoughts

Necessity became the mother of reinvention for the insurance industry, with many insurance carriers showing their adaptability and resilience during the last three years.

The “Great Resignation”. Hybrid working. Work-life balance. Purpose. Culture. As we emerge from the worst of the pandemic, these words have become ubiquitous in the debate about the “new normal”. While some may dismiss them as “clickbait”, the reality is that they signpost a significant shift in the way society, employers and their workforces have come to view the world of work.

Moving further into 2023, in setting strategic plans, investment priorities, and budgets, insurers should therefore strive to maintain the momentum of creative adaptation established over the past few years, accelerating upgrades in systems, talent, and culture while becoming increasingly proactive, innovative, and customer-centric.

At Landmark Underwriting we have adapted to this change and remain available wherever we or our stakeholders are. We value face-to-face interactions but also respond to the needs of remote working, especially in a global marketplace.

If you would like to get in touch, please contact:

Kate Albert – Head of Underwriting

k.albert@landmarkunderwriting.com

Chris White – Head of PI

c.white@landmarkunderwriting.com

Stefan Cole – Head of D&O

s.cole@landmarkunderwriting.com

Andrew Ravenscroft – Head of Property

a.ravenscroft@landmarkunderwriting.com